THE NEW AGE OF CLIMATE RESILIENCE Accelerating emergencies, misinformation, a faltering insurance market, and mutual aid: Welcome to the new Wild West of climate resilience. By Berit Anderson

Why Read: The LA wildfires have sparked a new era in climate resilience. While developers and financiers look to scoop up properties for redevelopment, individual homeowners - increasingly abandoned by insurers, under-supported by FEMA, and radicalized by a combination of misinformation, government red tape, and oligarchic indifference - are learning to save themselves. _______ "So do you really believe that in the future we're going to have the kind of trouble you write about in your books?" a student asked me as I was signing books after a talk. The young man was referring to the troubles I'd described in Parable of the Sower and Parable of the Talents, novels that take place in a near future of increasing drug addiction and illiteracy, marked by the popularity of prisons and the unpopularity of public schools, the vast and growing gap between the rich and everyone else, and the whole nasty family of problems brought on by global warming. "I didn't make up the problems," I pointed out. "All I did was look around at the problems we're neglecting now and give them about 30 years to grow into full-fledged disasters." - Octavia Butler, former Altadena resident, writing in Essence magazine (May 2000)

This past September, I flew into Los Angeles for a renewable-energy conference that brought 30,000 people to the Anaheim Convention Center. When I landed at John Wayne Airport, the hills ringing Anaheim were already on fire. As I waited for my Uber on the upper deck of the parking structure, the sky tinged grey and orange, I snapped a shot of the flames in the distance.

My fellow travelers seemed unphased, buried in their phones. At no point during the three-day conference did *any* of the professionals I met in renewable energy - ostensibly a crew that might care quite a bit about how the climate emergency is driving a significant increase in urban wildfires -mention the fact that the nearby hills were actively on fire. The main climatic difference between that day in early September and January 7, the day wildfires first swarmed through large swaths of habitable Los Angeles, was the rush of the Santa Ana winds, reported to have exceeded 80 mph as they fanned the flames in the hills above Altadena and Pacific Palisades. "Los Angeles weather is the weather of catastrophe, of apocalypse," Joan Didion wrote of the Santa Anas in Slouching Toward Bethlehem, "and, just as the reliably long and bitter winters of New England determine the way life is lived there, so the violence and the unpredictability of the Santa Ana affect the entire quality of life in Los Angeles, accentuate its impermanence, its unreliability. The winds shows us how close to the edge we are." Today, more than 50 years after the publication of that essay, the winds have, once again, shown Angelenos - and a watching world of other horrified urbanites who'd previously felt assured of the safety of their chosen cities by their close, concrete confines - how close to the edge they are. Were those same Anaheim hills I saw in September to ignite in flames today, Angelenos in the airport line would almost certainly, to quote LA resident and Hollywood director Adam McKay, "look up." And though the fierce Santa Ana winds themselves are not new to LA, the world into which they fanned this year's flames is not the same as the one Didion described so astutely all those years ago.

The Patterns of Climate Emergency Imagine, for a moment, the annals of the Microsoft Azure database that will be assembled to train future AI models about the human foibles of the Anthropocene era. Looking back at human and corporate responses to a worsening progression of the climate emergency, what patterns will we see? 1. An increased frequency of natural disasters - fires, floods, thunderstorms, hurricanes, and other windstorms - continuing to drive destruction in high-population areas.

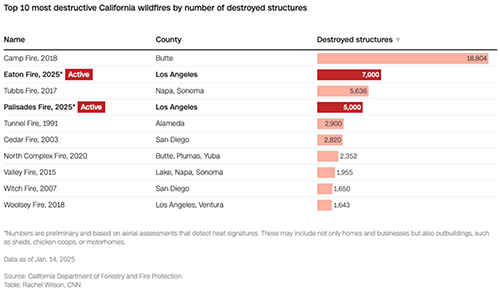

Source: AON 2. Increased size and scale of destruction from individual events. As the climate emergency progresses, individual weather events are causing more damage overall.

The LA fires are historic in scale, but California is by no means the only region dealing with accelerating impacts of larger storms. According to global insurance broker Aon's 2024 Climate and Catastrophe Insight report: Insurers across the world covered $118 billion, which was above the 21st century average ($90 billion), as well as the decadal mean ($110 billion). U.S. drought and the earthquake sequence in Turkey and Syria were the costliest events for insurance, considering both public and private entities. While no event reached the 10-billion-dollar mark, there were at least 37 billion-dollar disasters in total, marking a new historical record. This underlines the growing frequency of medium sized events, particularly severe convective storms, and their impact on global losses. Among those listed, fires were not the most costly category, but convective storms. What is a convective storm? Per JS Held, a global advisory services firm: According to Aon, severe convective storms have accounted for 70% of global insurance losses in recent years, and there continues to be a rise in such losses, largely due to growing exposure. In the US state of Texas alone, between January 1, 2012, and January 1, 2024, large hail originating from severe convective storms occurred an average of 197 days per year - more than in any other state. There was also an average of 49 days per year of at least one reported tornado, where Texas also stands as the leader, with 176 days on average of reported thunderstorm wind damage. 3. In the midst of each major natural disaster, a microcosm of information warfare then plays out over and over:

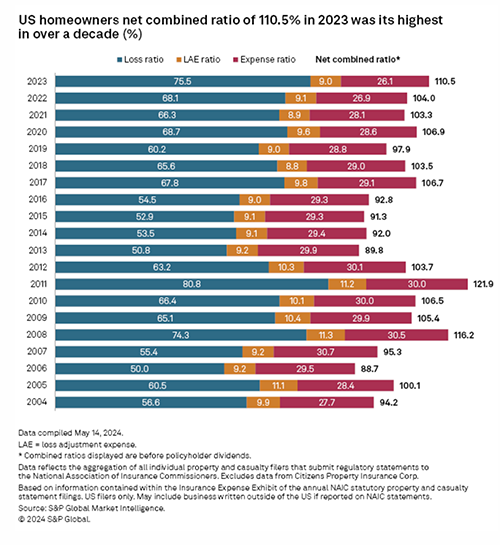

4. A decrease in individual homeowner wealth and assets in affected areas as lower- and middle-class people who can't afford insurance premiums or rebuilding are forced to sell their homes - now worth a fraction of their assessed value. As reported in the Los Angeles Times: It's not clear how many homeowners in Pacific Palisades and elsewhere might not have had coverage, but many homeowners reported that insurers had not renewed their policies before the disaster struck. State Farm last year told the Department of Insurance it would not renew 1,626 policies in Pacific Palisades when they expired, starting last July. Even those who did have insurance face a long uphill battle: the levels of toxicity in entire stretches of LA will be unprecedented. The road to remediation and re-permitting will likely be in the range of a decade, not just a few years. Those lucky residents whose homes didn't burn are still left with a functional home in the middle of an apocalyptic wasteland. As reported in CalMatters: "Think about all the things in a house," said David Hornung, who oversaw Occupational Safety and Health's response to the Tubbs Fire that ravaged the Sonoma County town of Santa Rosa in October 2017. "There are televisions, electronics, dishwashers; it's really complex." Computers and other electronics contain lead, mercury, arsenic and other dangerous chemicals. "Then you have plastics and composite material," which may release hydrochloric acid, sulfur dioxide and heavy metals when burned. "You get a real complex mixture of chemicals." Already, I'm hearing about plans to move from those whose homes survived the fires - even those not directly in the fires' paths. They don't want to risk spending the next few years slowly poisoning themselves or their families with carcinogens. The November 2018 Camp Fire in Paradise, California, offers a lesson in the best-case scenario for this kind of thing: a revival of homes powered by more than $1B in state and federal assistance - not to mention a $220 million PG&E settlement. But even there, where houses have been rebuilt according to strict fire codes and without wooden porches, where power lines have been diligently buried to reduce risk, recovery has been slow. New York Times reporter Mark Arax traveled to Paradise in November 2023, visiting with construction workers who still lived there: "The population has fallen to around 9,000 from roughly 26,000," he reported. Now, [town official and recovery manager Colette] Curtis said, Paradise didn't have enough tax-generating houses and businesses to cover its old operating budget of $11 million. Before the blaze, the town numbered 12,000 homes and 1,500 businesses. Today, there's not quite 4,000 houses and 450 businesses. To keep Paradise afloat when the PG&E money runs dry in 20 years, it'll take at least a doubling of both. This will necessitate a decade and more of nonstop building. Among those who stayed, insurance premiums are now unspeakable: one resident, who managed to protect his home during the fire with a single garden hose and buckets filled from his pool, was at the time of Arax's visit paying $8,400 a year for insurance. 5. An upswing in demand, prices, and profits for remediation, construction, and construction-related entities. The construction business in LA - already a tight one - is about to boom. It's a great time to own a hardware store, a lumber supply yard, or a concrete business in the LA area. But all that won't likely pick up for the next year or so. The remediation of Paradise took 9 months and 3,000 workers in hazmat suits - who removed 3.6 million tons of debris. That's more than twice as much as was removed from the site of the World Trade Center. 6. An increase in corporate assets in affected areas among developers and developer-related entities. In some cases, this may also be an opportunity to develop larger-scale projects. It will be years before any large-scale plans take shape, but the decimation of an entire region also brings with it the potential for land grabs - the chance to construct something much bigger than a standard-sized residential or commercial parcel. 7. A continued decline in the commercial viability of the insurance model and an increase in rates. As S&P Global reported earlier this year, the overall home-insurance industry is in deep trouble, with its loss ratio now consistently hitting new highs since at least 2016: In an attempt to return to profitability, insurers have been boosting rates across the US; however, net underwriting losses within the homeowners business line were about $15 billion in 2023, compared to $5.89 billion during the previous year. The underwriting performance figures exclude state-backed insurers of last resort, such as Florida's Citizens Property Insurance Corp.

In other words, these numbers don't even include those institutions set up to take on the "worst of the worst" risk - those properties deemed uninsurable by traditional home insurers. This means that overall, we can expect premiums to keep increasing across the US. Interestingly, there are a few outliers to this pattern - notably Chubb, which insures primarily high-net-worth individuals. With a net combined ratio of 89.6% in 2023, roughly one-third of its premiums come from mid-Atlantic states. Which brings us to the final pattern here: 8. The disappearance of insurance availability in areas of extreme financial pressure. California, which recently passed mind-boggling regulations on insurance premiums, will be first in line. As the Cato Institute describes: California's price controls, whereby regulators must approve proposed premium increases, require insurers to submit detailed justifications for their rate increases to the California Department of Insurance (CDI). Crucially, those companies have until recently had to demonstrate that proposed premiums are based on historic losses, not analysis based on forward-looking risk assessments. Unless something changes here, we're going to see those companies that still provide insurance in California continue to opt out rather than operate at an extreme loss for the foreseeable future. If that happens, it will spell trouble, as well, for the state insurance schemes in Florida and California. Those programs rely on fees from traditional insurers operating in the state in order to provide coverage for properties normal home insurance won't touch. A December Senate Budget Committee report entitled Next to Fall: The Climate-Driven Insurance Crisis Is Here - and Getting Worse shared a dire warning: This is predicted to cascade into plunging property values in communities where insurance becomes impossible to find or prohibitively expensive - a collapse in property values with the potential to trigger a full-scale financial crisis similar to what occurred in 2008.

The Myth of the Rugged Individual If there's one thing that the burning of a major metropolitan area shows, it's the positive side of human nature. Humans will - and do - take things into their own hands, especially as they see a gap between traditional institutions and what needs to be done to keep themselves, their families, their homes, and their neighbors safe. In LA, we're seeing this play out in myriad ways. WhatsApp, Nextdoor, GoFundMe, and Facebook as tools of resilience. Regional social-network groups and communication platforms like these are the digital backbone that facilitate community resilience. Widespread and easy-to-use, they facilitate near-seamless, bottom-up organizing, allowing residents to communicate en masse in the face of quickly changing conditions. Take, for example, Edgar McGregor, a recent meteorology and climate-science graduate living at home with his parents in Altadena, who ran an Altadena Weather and Climate group on Facebook dedicated to providing neighbors with updates about the micro-climate in their neighborhood. As a close observer of the Eaton Canyon area he issued a stark warning to his followers in the leadup to the fire, warning them to evacuate. A poll in that group indicates that over 800 people did so at his suggestion, allowing them to get out of the area safely. One commenter wrote: "We live in La Crescenta, and because of his seriousness regarding the coming wind storm, we also packed Tuesday evening. We received our evacuation warning Wednesday morning and left immediately. Yes, he definitely affected our decision." Another weighed in: "I started reposting this page's information on What's Up In Altadena about 10 days before the fire. [...] and amped up the two days before. Because of what he posted, I knew to get out as soon as I heard of the fire. I warned the 18,000 readers to go, or be ready to go." A Wall Street Journal article this week included an interview with Altadena residents bucking police orders and sneaking behind barricades to access their homes and protect those of their neighbors: [Pacific Palisades resident Ross] Gerber and his neighbors have turned to their community WhatsApp, which had been used largely to air minor gripes about traffic and such. Now, it is an organizing tool, he said, "better than any government." He had long been skeptical of the system, he said, but the fires further showed him that communities need to be prepared to fend for themselves. Left to their own devices, humans will come together. As climate destruction increases, and insurance becomes less dependable and more expensive, homeowners and citizens will increasingly self-organize to protect their interests. Mutual aid distributed via Cash App, Venmo, and GoFundMe is already beginning to act as supplemental insurance in emergency situations - especially in communities where premiums have increased or families are not insured. For many, this has been an essential tool to keep them on their feet, allowing them to find temporary shelter while they begin to navigate insurance claims. An increase in individuals' reliance on personal preparation to protect personal property. Across the country, forest management has been hamstrung by regulations limiting the Forest Service's ability to lead controlled burns. As Ben Krauss at Slow Boring reported last June, the "Cottonwood decision" - named after an environmental center that sued the Forest Service to protect the habitat of the Canada lynx and other endangered species - made it a requirement that the Forest Service pause all of its forest management plans whenever new information about endangered species in the area arises. A temporary stay on that rule expired last year. As reported by Krauss: But even if the Cottonwood decision is reversed, the simple truth is that under the current environmental review process, the Forest Service isn't going to be able to accomplish their goal of treating 50 million acres of forest by the coming decade. According to PERC, it takes nearly five years to begin a prescribed burn through the environmental review process. For projects that require environmental impact statements, that process can jump up to over seven years. Dwyer told me that the organization is "not against the environmental review process. It's well intentioned." However, as the report notes, these dramatic delays must be reformed if we're going to have a chance at removing the excess forest build up that is driving a lot of these forest fires. In a recent interview with the Los Angeles Times, wildfire expert Jack Cohen explained how homeowners focusing on their own neighborhoods might have the best chance of avoiding the spread of fire in urban areas: In high-density development, scattered burning homes spread to their neighbors and so on. Ignitions downwind and across streets are typically from showers of burning embers from burning structures. suggests the following: Houses are much more resilient to fires if they have no vegetation within 5 feet of the house, and vegetation is fire-resistant and sparse from 5 feet to 100 feet. Building codes and "home hardening" also make a difference. Things like non-combustible roofing materials (e.g., metal, tile, or asphalt shingles), ember-resistant vents with mesh screens, and fire-resistant materials for siding (like stucco, fiber cement, or metal) have been shown to be effective in the lab as well as real-world settings. Landscaping used to be a point of pride, an asset. Now it's a liability. But per Brown's advice and Cohen's warning, it's not enough for individual homeowners to make repairs. In urban areas, especially, your home is only as safe as the other homes in your neighborhood. Whether or not you live in an area at high risk for fires, we are all close to the edge. (I could see insurance companies offering breaks in premiums for neighborhoods where a certain percentage of homes have completed necessary fireproofing.) The risk to homes and property from climate-emergency-induced weather patterns is here. It's not going anywhere. And our ability to navigate it will rely on our ability to organize as individuals. But beyond our personal resilience, there is another essential step we can take to slow all of this: transitioning to a fully renewable economy. As the insurance industry makes clear, these disasters are accelerating, in both their frequency and the destruction they leave in their wake. The only way out is through. And the deployment of renewable systems, energy storage, and microgrids - as FAST as we can expand them - is our best shot at mitigating climate-related disasters. We have the tools; we have the technologies. The only thing in short supply is time. So let's get to work.

Your comments are always welcome.

Sincerely, Berit Anderson

DISCLAIMER: NOT INVESTMENT ADVICE Information and material presented in the SNS Global Report should not be construed as legal, tax, investment, financial, or other advice. Nothing contained in this publication constitutes a solicitation, recommendation, endorsement, or offer by Strategic News Service or any third-party service provider to buy or sell any securities or other financial instruments. This publication is not intended to be a solicitation, offering, or recommendation of any security, commodity, derivative, investment management service, or advisory service and is not commodity trading advice. Strategic News Service does not represent that the securities, products, or services discussed in this publication are suitable or appropriate for any or all investors.

We encourage you to forward your favorite issues of SNS to a friend(s) or colleague(s) 1 time per recipient, provided that you cc info@strategicnewsservice.com and that sharing does not result in the publication of the SNS Global Report or its contents in any form except as provided in the SNS Terms of Service (linked below). To arrange for a speech or consultation by Mark Anderson on subjects in technology and economics, or to schedule a strategic review of your company, email mark@stratnews.com. For inquiries about Partnership or Sponsorship Opportunities and/or SNS Events, please contact Berit Anderson, SNS COO, at berit@stratnews.com.

Ed. Note: Some letters may be republished to include subsequent replies.

Subject: Fw: Have you seen this? Evan and Mark, Hi! Happy New Year! Have you seen this? Biden-Harris Administration Announces Regulatory Framework for the Responsible Diffusion of Advanced Artificial Intelligence Technology [Bureau of Industry & Security] Reminded me of our discussion on your predictions call re US increasing export controls to help protect US advances in AI.

Jody R. Westby, Esq. CEO, Global Cyber Risk LLC

Jody, Wow. This is going to be extremely hard to define and control. Sounds like a wish list, more than something that can actually be gauged in a courtroom or boardroom.

Mark Anderson

Mark and Evan, Agree. Here is another good article on it. What to Know About the New U.S. AI Diffusion Policy and Export Controls [Council on Foreign Relations]

Jody Westby

Jody, Thank you. I like the spirit, but have no idea how it would work. How do you keep China from getting cloud access to tech?

Mark Anderson

Jody and Mark, Yeah, that's a tough one. We might need to start actually preventing them from hacking all of our networks and devices in order for it to work. :) It's a good start though, with a lot more to be figured out. They will also surely game out using pass throughs via other companies and nations, so its whack-a-mole for the time being anyway, but this enables that process to begin.

Evan Anderson

Subject: Breaking news: South Korea's acting president and prime minister is impeached [To SNS Asia Editor Scott Foster] Scott, So then there's this ... (wha'?). I wonder if you'd consider writing an Ethermail on the topic. No expectation. South Korea's Acting President and Prime Minister Is Impeached Opposition lawmakers in South Korea voted to impeach the prime minister and acting president, Han Duck-soo, in the latest turn in a political crisis that has created a power vacuum in the country. And: Thank you for this year's-end Asia Letter. It was one of your best, imho. And: Are you familiar with Christopher Yomei Blasdel? I inherited a stack of CDs from Sam Hamill, and came across him tonight while deciding which to keep. (This won a place.) The album notes lead me to imagine you may know him - "Night of the Garuda."

Sally Anderson

Mark and Sally, As a follow-up to my recent SNS Asia Letter: The impeachment of South Korean Prime Minister and acting President Han Duck-soo less than two weeks after the impeachment of President Yoon Suk Yeol demonstrates both the power of the leftwing Democratic Party of Korea (DPK) in the National Assembly, the weakness of the conservative People Power Party (PPP), and the highly emotional disruption of government in Seoul. The vote was 192 to zero as the conservatives walked out, protesting that impeaching a president requires a two-thirds majority. But impeaching a prime minister requires only a simple majority and the assembly ruled that since Han was appointed and is only the acting, not an elected, president, a two-thirds majority was not required. Deputy Prime Minister and Finance Minister Choi Sang-mok will be the next acting president, with no guarantee that he, too, will not be impeached. Meanwhile, although Yoon's powers have been suspended, Seoul-based military historian and journalist Andrew Salmon reports that "He is not communicating, appearing or responding to police summonses." After reviewing the overall situation, Salmon concludes that "This means a key U.S. Indo-Pacific ally and pivotal node in global supply chains is sailing into uncharted political waters." Grounds for impeachment included Han's alleged stonewalling of the appointment of three new judges to Constitutional Court, which will rule on the validity of President Yoon's impeachment (three of the court's nine seats are now vacant), his alleged involvement in Yoon's attempt to impose martial law, his veto of a special investigation into the allegedly corrupt activities of Yoon's wife, and conniving with PPP leadership to share power. DPK leader Lee Jae-myung referred to Yoon and his colleagues as "rebellion forces" and said, "We will mobilize all resources and fulfill our historical responsibility until Yoon Suk Yeol is removed from office, his loyalist forces are eradicated, and the rebellion is fully suppressed." Recall that President Yoon told the nation that "I am declaring a state of emergency martial law to protect the free Republic of Korea from the threats of the North Korean communist forces, to eradicate the shameless pro-North anti-state forces that plunder the freedom and happiness of our people and to safeguard the free constitutional order." In other words, the two sides in this extremely vibrant democracy are calling each other traitors. Immune to irony, a U.S. State Department spokesperson told the Yonhap News Agency that, "As the Secretary [Secretary of State Anthony Blinken] said, the most important thing is that the Republic of Korea has demonstrated its democratic resilience." "We strongly support the ironclad alliance that joins our two countries together and that's done so much over the last few years," the spokesperson continued. "In recent years, that Alliance has made enormous strides, and the United States looks forward to partnering with the ROK [Republic of Korea] on achieving further progress." We will soon see how different Lee Jae-myung and Donald Trump's ideas of progress are, both to those of the Biden administration and to each other's. [P.S.] Sally: I hadn't thought about him for quite some time, but Christopher Yomei is well known in the shakuhachi world. Not our group, though. Night of the Garuda is pretty good. Never heard it before.

Scott Foster Journalist, Asia Times

Scott, Well done as always. We have two impeached SK leaders on the run, and now a past Taiwanese president headed for jail. A new PM in Japan, and - Anthony Albanese. Uh Oh.

Mark Anderson

Mark & Sally, The third-party Taiwanese presidential candidate, Ko Wen-je, received more than 25% of the vote, allowing rightwing China-hating Lai Ching-te to become president with only 40%. If he goes to jail ,,, I will ask some people who know more than me about Taiwan what this might lead to, but you can guess. Here in Japan, the right wing of the LDP is doing whatever it can to sabotage Prime Minister Ishiba, who is doing a fair job of working with the opposition. They want to bring back stable one-party government, but that doesn't seem likely. Happy New Year !!!

Scott Foster

Subject: Happy New Year Happy New Year, Mark, Berit and Sally (and Evan, whose email I don't have). It was a pleasure spending time with you in 2024, participating in FiRe and seeing Pattern charge ahead, reading SNS newsletters, and getting to meet some of your friends and associates. I hope to see more of you in 2025, assuming that the world doesn't end. What a productive, interesting bunch you all are. Love from me and my family,

John Payne Ecologist | Data Scientist

John, (I've added Evan, so now you have his address.)

Thanks so much for this fine and eloquent greeting for the New Year, and for your kind words ... We would all be delighted to see more of you and your family, in 2025 or any time at all, given that we survive. It would be reason to celebrate together, wot? Coincidentally, just a few days ago I sent Mark and Sharon (Mark's and my younger sibling, FiReFilms CEO and former FiRe programs director, who couldn't to make it to FiRe last year) this photo of we three with your dad in Park City. This was in 2014, on the occasion of Roger presenting at the SNS-FiRe-Park City Institute Speaker Series, which series was started and hosted by Sharon. We all spent the weekend together at her home [. . .] where most of us will be meeting soon for a belated celebration of Christmas and family, towering snow drifts, and near-Arctic temperatures. Please give our love to everyone, and let me know what you're all up to these days. We likely have overlapping connections, between the environment at large, marine mammals, interspecies communication, and documentary film. Warmest.

Sally Anderson

Subject: Re: Happy Holidays Berit and Mark, Many thanks for all you do!! Happy Holidays and best wishes for the new year to you both!

Randy Blotky CEO

Randy, Thank you, and our very best to you and your family. You're a highly valued member of our own extended family, and we're grateful for your contributions and presence in this circle of care.

Mark Anderson

Subject: Re: "SNS: The Risk Window: Government Transitions & Disarray in the Next Six Months" Damned fine article, Evan - you are an equal to your dad. But for god's sake, don't tell him that; he might want to retire.

Scott Biddle [Roche Harbor, WA]

Scott, Haha, thank you! [. . .] I hope to see you soon.

Evan Anderson

Copyright 2025 Strategic News Service LLC "Strategic News Service," "SNS," "Future in Review," "FiRe," "INVNT/IP," and "SNS Project Inkwell" are all registered service marks of Strategic News Service LLC. ISSN 1093-8494 |